ubia of qualified property

Commonly qualified property is any tangible property that is used in the trade or business and. They need to report the W-2 wages and UBIA of qualified property uh from the trade or business They need to report any qualified REIT dividends and qualified PTP income coming through.

|

| Qbi Unadjusted Basis Immediately After Acquisition Ubia |

This figure is routinely used in the calculation for the Qualified Business Income Deduction.

. The UBIA of qualified property. Publication 535 defines the Unadjusted Basis Immediately after Acquisition UBIA as the basis of the qualified property on the placed-in-service date. Publication 535 defines the Unadjusted Basis Immediately after Acquisition UBIA as the basis of the qualified property on the placed-in-service date. The taxpayer receiving the qualifying property in a step-in-the-shoes transaction determines the placed-in-service date for the property using a two-step approach as defined by the regulations.

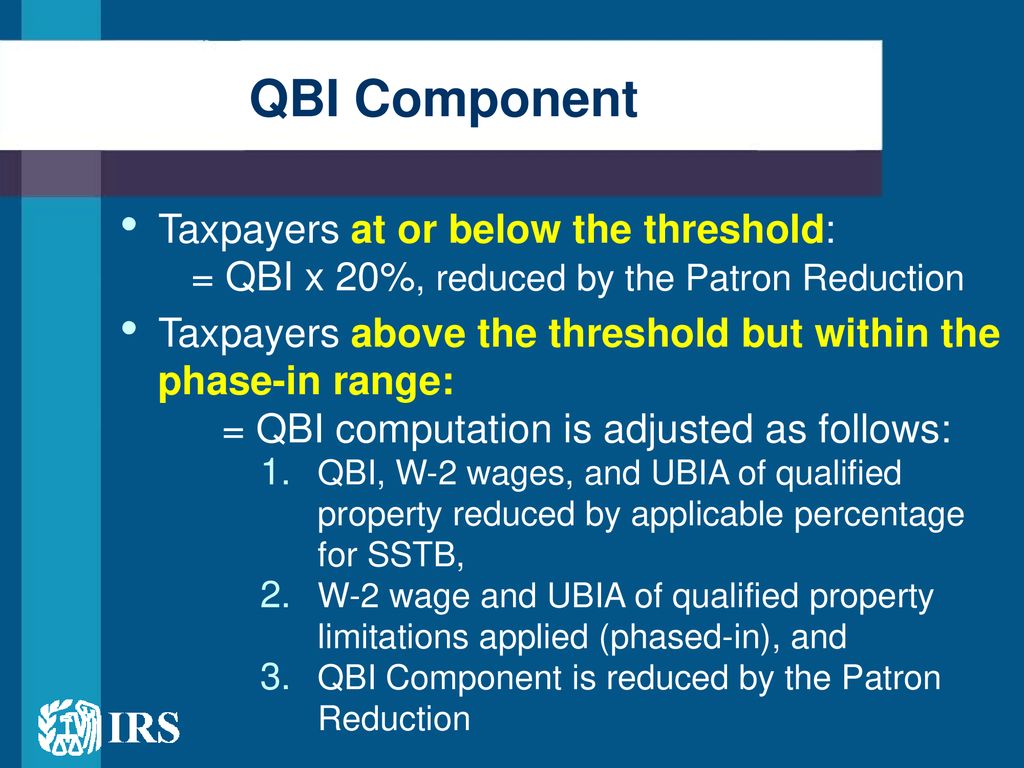

A taxpayers UBIA of qualified property is its basis in the qualified property prior to any adjustments under section 1016 a 2 or 3 any adjustments for tax credits you or the RPE. UBIA of qualified property 3 UBIA of qualified property - Source. Section 199Ab2Bii provides an alternative deduction limitation based on 25 percent of W-2 Wages with respect to the qualified trade or business. UBIA highlighted in red of this 380 amount.

26 CFR 1199A-2. Qualified Property includes depreciable. UBIA refers to Unadjusted Basis Immediately after Acquisition. 199A Sum Wks - UBIA - The Total Amount is Larger than the amount allocated to all Schedule K-1s.

Qualified property includes tangible property subject to depreciation under section 167 that is held and used in the production of QBI by the trade or business or aggregated trades or. When calculating UBIA discussion centers around what is considered qualified property. At the end of year 1 MNOP has 100000 of UBIA in qualified property which is allocated among the partners equally. However on June 30 of year 2 P sells 100 percent of its interest to Q in an.

Qualified Property includes depreciable.

|

| Irs Provides Qbi Deduction Guidance In The Nick Of Time |

|

| What You Need To Know About The 199a Pass Through Deduction |

|

| Irs Provides Qbi Deduction Guidance In The Nick Of Time Mauldin Jenkins |

|

| Irs Provides Qbi Deduction Guidance In The Nick Of Time Blue Co Llc |

|

| Insights Into Section 199a Operational Rules |

Posting Komentar untuk "ubia of qualified property"